A deep look at how the payday loan industry is able to keep advertising despite Google’s policy changes.

To consumer advocates, payday loans have become synonymous with predatory lending. The small short-term loans often come with astronomical interest rates that can pull consumers who are trying to get by from paycheck to paycheck into a deepening hole of debt.

Just this week, the FTC fined a payday lending group $1.3 billion for deceptive loan practices. Industry watchdog groups have been advocating for more regulation and pressing for change, and in May, Google announced it would start to ban payday and high-interest loan ads.

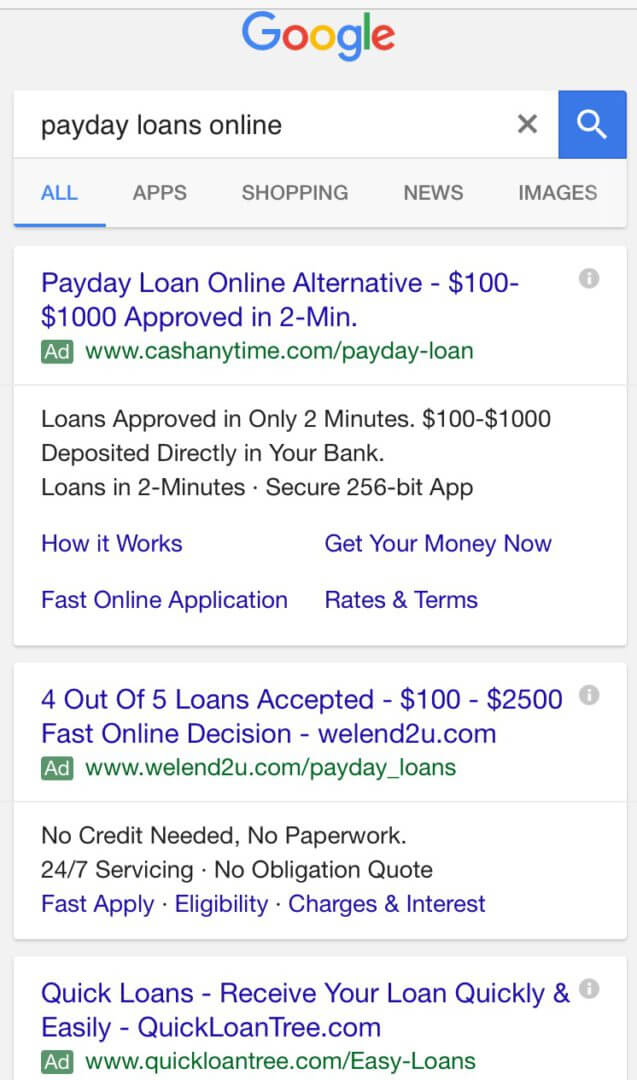

The ban started rolling out the week of July 20. There were estimates the move could cost Google millions in lost ad revenue. Yet, more than two months later, it appears the ban is likely having little to no impact on Google’s bottom line. as ads continue to fill the available slots on desktop and mobile. Why? Because it’s not an actual ban, and the advertisers quickly figured out how to change their messaging to meet Google’s policies.

In a review over the past month, I have found advertisers showing messaging on landing pages from Google ads that complies with the new restrictions (APR rates no higher than 36 percent and minimum repayment period of 60 days). But the fine print shows the ranges shown on the landing pages are essentially just a way of getting around payday loan policy. And fine print isn’t the only way the companies are evading the rules.

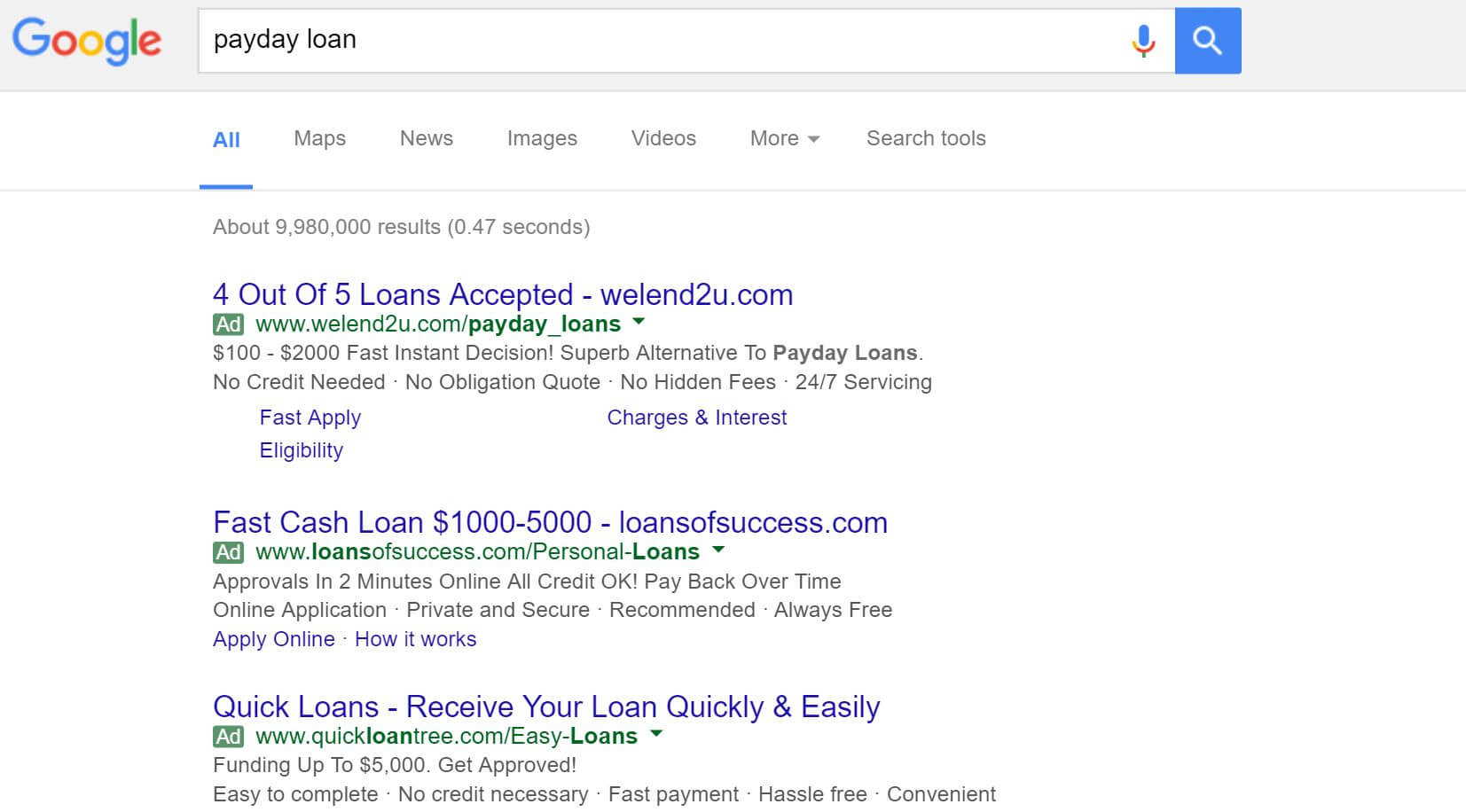

Non-Direct lenders aren’t responsible for actual APRs

With very few exceptions — Discover Personal Loans and CashNetUSA being two — the advertisers are lead generators, or loan brokers, which means they aren’t doing the actual lending. By being one step removed from the actual lending process, these advertisers can list terms that fall within Google’s payday loan policy on their ad landing pages without having to actually be beholden to those terms.

The terms listed on the landing pages (often in fine print at the bottom of the page) from the lead generators’ advertising varies, but often you’ll see some terms that fall within the range of Google’s policy, but when read carefully, make clear that the actual APR could vary outside that range (i.e., higher). Here are just two examples (bolding is mine).

From LoansOfSuccess.com:

“LoansOfSuccess cannot guarantee any APR, since we are a lending network. Though a Representative APR can range between 5.99–35.99%. The Maximum APR is 35.99. When accepting a loan from a lender, the lender can provide a different APR than our range. Please check the loan disclosure before approving and signing the agreement for your loan.”

From WeLoan2U.com:

“Consumers, who qualify with a lender, can be offered loans with APRs below 36% and have payment terms ranging from 61 days to 60 months, or more. Cash transfer times may vary between lenders and may depend on your individual financial institution. For details, questions or concerns regarding your loan, please contact your lender directly.”

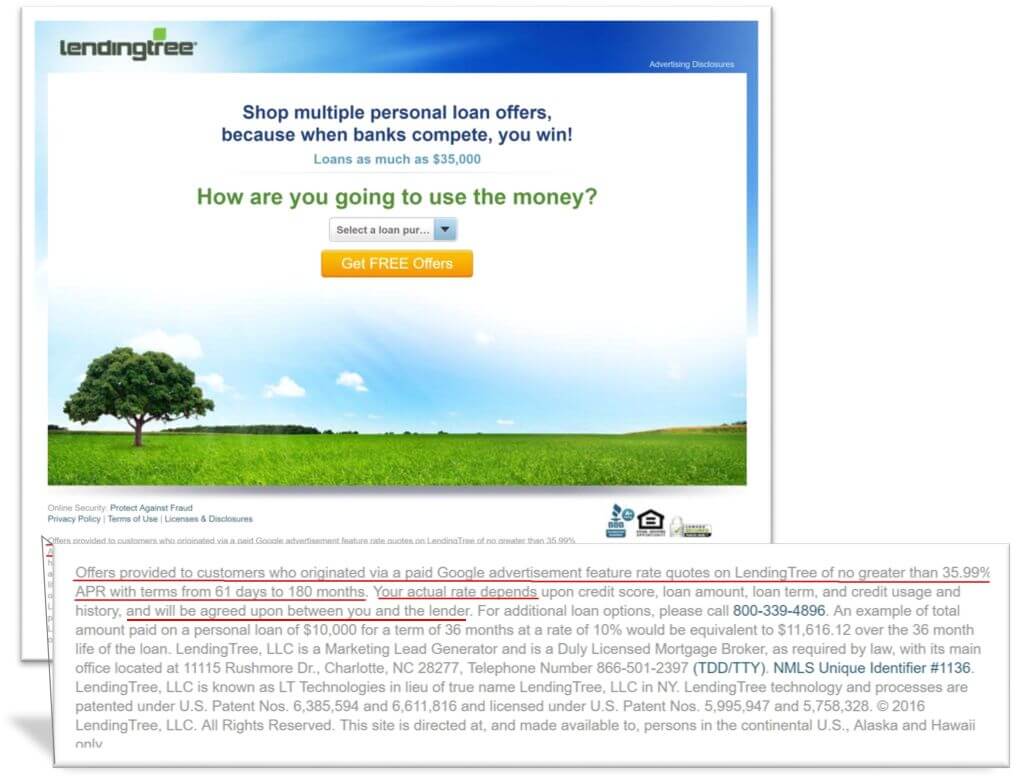

LendingTree took this a step farther by explicitly stating on its landing page that because I clicked through “via a paid Google advertisement,” the offers I’ll see on LendingTree will feature quotes “of no greater than 35.99 percent APR with terms from 61 days to 180 months.” Sounds great, except “Your actual rate depends … and will be agreed upon by you and the lender.”

[Click to enlarge]

When I called to ask LendingTree if the loan offers I might receive from lenders could potentially be higher than the 35.99 percent APR listed on the landing page, a representative said that the loan rates “shouldn’t be higher than that limit shown, but could be because the rates are up to the the lenders.”

QuickLoanTree.com lists APR terms stating “the maximum Annual Percentage Rate (APR) is 35.99%,” yet adds that “the lender can provide a different APR than our range.”

provides the capital for CashNetUSA loans.

provides the capital for CashNetUSA loans.

This call-only ad from personal-loan.phoneloans.com connects to a CashNetUSA call center.

This call-only ad from personal-loan.phoneloans.com connects to a CashNetUSA call center.

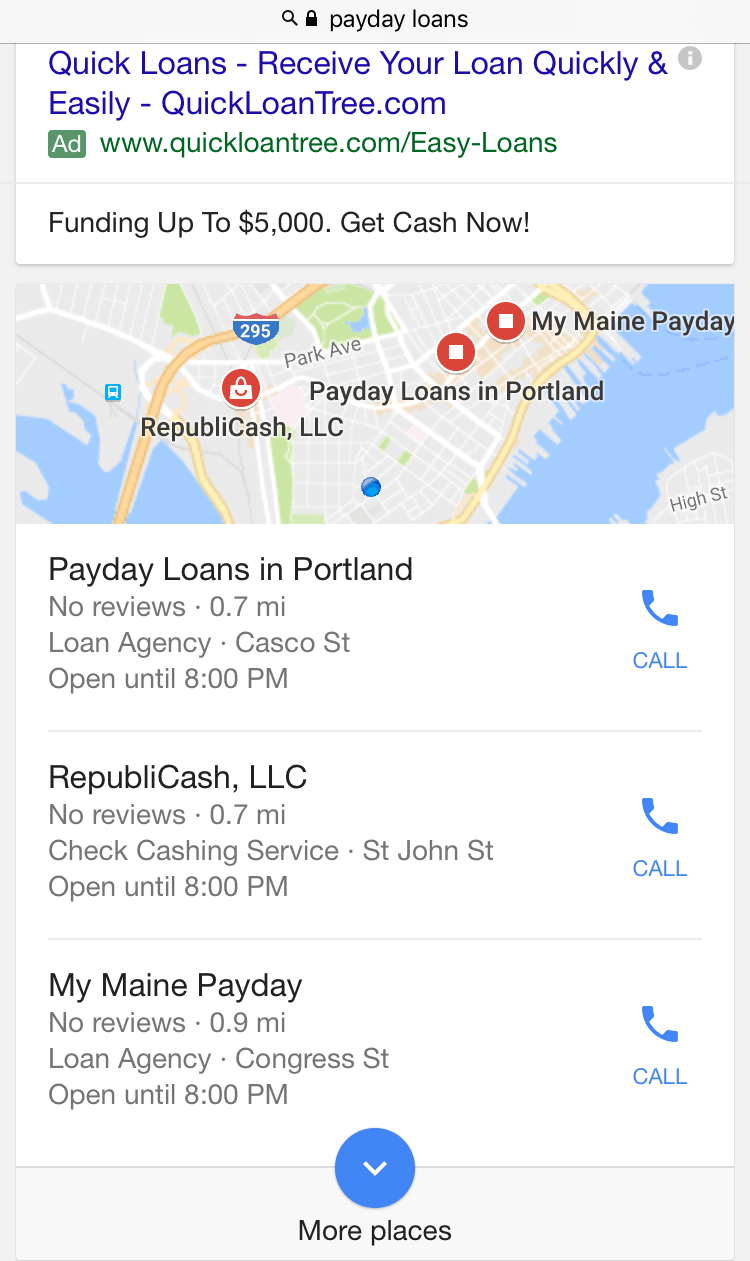

While not specifically ad related, the other area where I found CashNetUSA using less-than-transparent practices is in Google Maps. Google Map Maker allows anyone to add a business to Google Maps, and the feature can be abused.

When I search for “payday loans,” the local pack of results in my area displays one verified location for RepubliCash and two unverified listings that look like Google Map Maker spam.

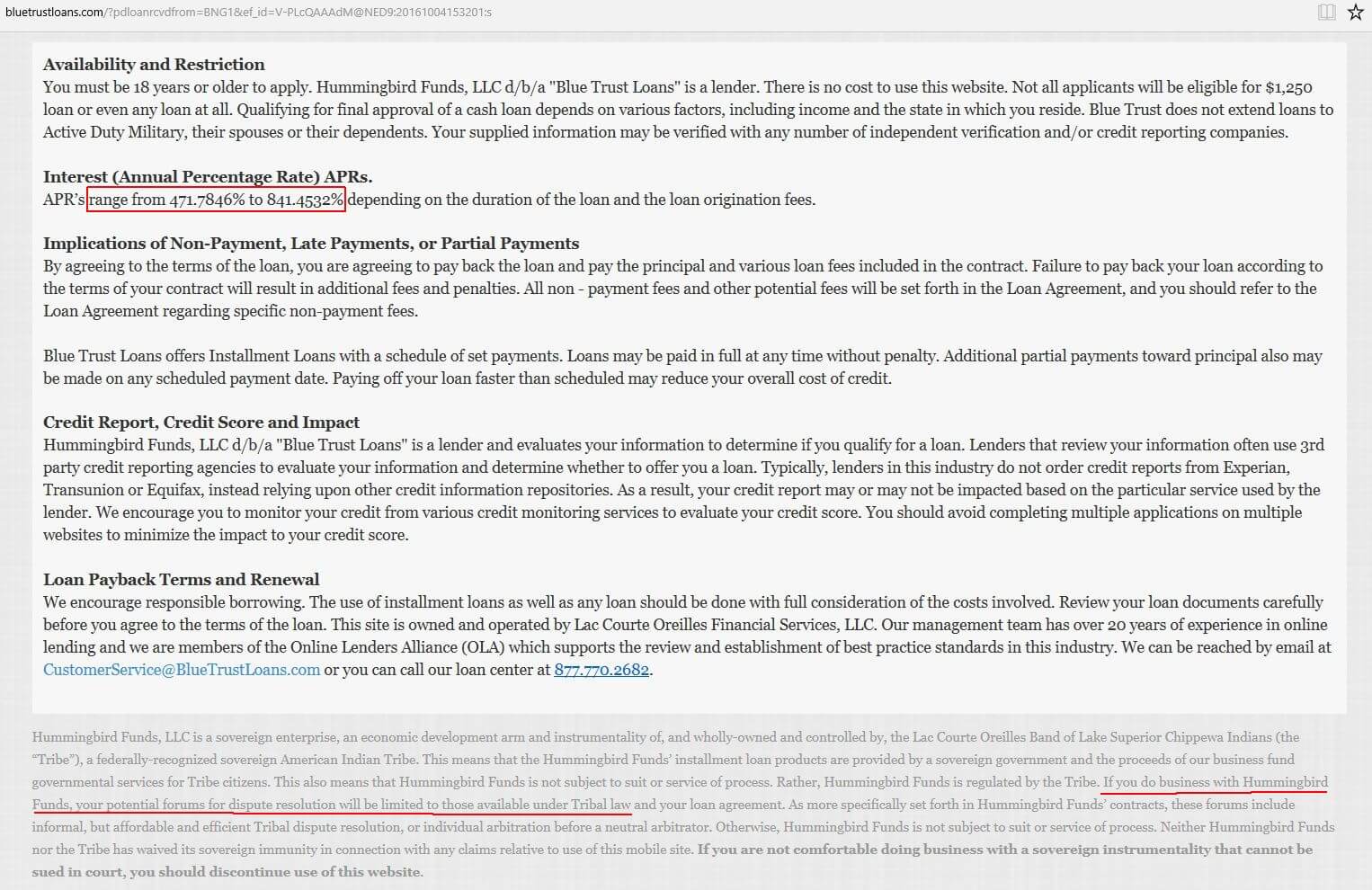

[Click to enlarge]

[Click to enlarge] financial products policy

financial products policy

{kind=link}